Definitions

SMP : System Marginal Price from which the wholesale price of electricity is derived

System Load : Electricity Demand for All Ireland system

SMP : System Marginal Price from which the wholesale price of electricity is derived

System Load : Electricity Demand for All Ireland system

All sorts of claims are made by all parties on the effects of wind energy on wholesale prices. Let's have a look at two recent days - 2nd and 23rd February - to see what impact, if any, wind energy has on wholesale prices. We can see that the demand for both days is very similar with a slightly higher peak on the 2nd.

.png) |

| Demand Profiles for both days for the Republic of Ireland only (information not available for All Ireland) |

.png) |

| Wind generation profiles for both days (Republic only)

On the 2nd, we can see that the average price was around € 50 with a peak price of about € 260

(Data taken from SEMO market data). |

On the 23rd, the average price was also about € 50 with a lower peak price of approx € 210. The higher peak price on the 2nd may well be due to the higher peak demand (load) or lower wind

on the 2nd or indeed a combination of the two.

But the important thing is that on average, prices for both days were remarkably similar at about €50 per MWh. What has happened in both cases is that the cost of gas generation, rather than wind, has determined the price. The ESRI graph below confirms that the price of gas comes in around the € 50 mark.

Let's take 2 different days - one with wind providing 1,000MW and another with zero wind. Demand is 4,000MW for both days. The marginal cost of generating a MW of gas power at 3,000MW on the windy day is the same as the cost of generating the last MW at 4,000MW on a calm day. So what we

will see is that both days, like in the above case, will have very similar or same market prices.

ESRI explain how the wholesale electricity price is determined :

The most expensive plant needed to meet demand sets the marginal price,

which is paid out to all generators producing electricity during that period.

The marginal price essentially reflects the cost of fuel and carbon needed to

generate the last MWh of electricity.

Since wind generation is assumed to have a short-run cost of zero, more

wind tends to put downward pressure on electricity prices, up to a point. Wind

generation is by its own nature variable. When wind dies down thermal plants

(typically fuelled by natural gas or coal) must be available to pick up the slack

in order to maintain a reliable electricity system. It takes several hours for a

thermal plant to warm up to the point where it can generate electricity. To

take this feature into account, we assume that a certain number of thermal

plants must always be on at their minimum stable capacity. The number of

plants that are constrained on depends on the time of the year and the level of

electricity demand and is determined on a monthly basis by the model. When

thermal plants are constrained on and would not otherwise have been dispatched

by the market, they do not bid their marginal cost into the market;

rather, they are compensated for this generation through constraint payments

which equal their marginal cost, regardless of market prices. At times the

need to constrain on thermal plants to maintain reliability might also cause

the curtailment of available wind generation. Wind curtailment is recognised

by the system operators to be a likely event (EirGrid and SONI, 2010).

The above diagram shows the merit order with which each type of generation is taken.

If gas becomes cheaper than coal, then it will move down the merit order and be chosen before coal. But at the moment mid-merit gas usually generates the last MWh of electricity. Hence, why the market price is usually based on the gas price. We can see from the below Eirgrid document that the System Marginal Price (SMP) does indeed follow the Gas Price :  |

The Energy Regulator agrees with Eirgrid on the impact of gas prices on wholesale

prices (PSO Paper) : The lower estimated wholesale price for next year is reflective of a trend in recent months in the SEM of lower spot and forward contracting prices, related to lower gas prices. But there may well be situations where high wind penetration coincides with peak demand during winter months. In this situation, wind could prevent peaking units from been used. Peaking units include oil and open gas cycle generators and are the most expensive form of generation hence why they are last in the merit order. In this situation, wind will bring down the wholesale price as it would prevent the market price from been derived by the high price bid by these peakers.

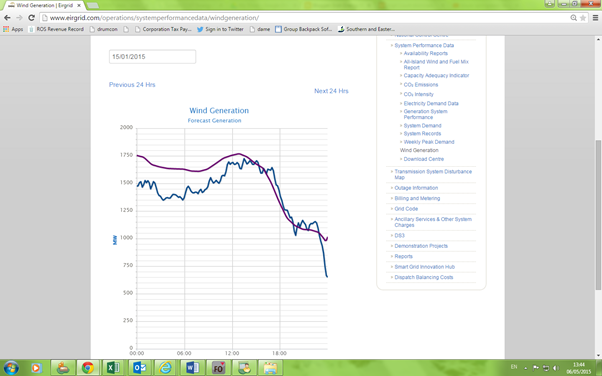

But likewise, there will also be times when wind output will fall off quickly resulting in the need

for quick acting peaking units like oil or ocgt to step in pushing the market price upwards. This is what may well have happened on the 15th January 2015 :

So to conclude, there will always be some form of gas generation in the system regardless of how

much wind is allowed in (due to system and balancing constraints). There may be slight reductions in the wholesale price where mid merit gas plant is prevented from been taken but as can be seen in the example above even with circa 1,700 MW of wind, mid merit plant is still required to balance the grid. There may be occasions when wind prevents expensive peaking plant from been taken but there will also be occasions when sudden fall offs in wind power require expensive fast acting expensive plant to fill the gap. If anybody wants to submit an article on how wind energy does reduce wholesale prices, then please

send to irishenergyblog@gmail.com and I will be happy to publish it.

But I will finish with an interesting question - what will happen the wholesale price if say, 75% wind is allowed into the system ? At this level, back up gas plants will be running on low loads, and potentially burning more fuel than if running more efficiently at higher loads. This will mean that the cost of providing the last MW of gas power will be more expensive than in the little or no wind scenario. So will we see upward pressure on the wholesale price in this case ? |

The wholesale price is irrelevant. The fundamental issue for all businesses is their ability to recover costs generated in supplying a product or service.The wholesale price is irrelevant if it does not do this.It is quite clear that the wholesale cost is inadequate for wind production to recover their costs. From here on wind will reduce the wholesale cost as surpluses generated will increase.This will reduce or eliminate margins for non wind generation and for wind to recover their costs non production related income will have to increase. With the massive capital investment required for wind generation and with smaller market opportunities for this added capacity the only way wind investments can remain solvent is to increase the PSO. The only thing that I see that may reduce the impact of these massive likely increases is the fact that these larger wind turbines are a load of junk and will have relatively short lives. If the Tories form a government in the UK wind in Ireland is dead. No interconnectors will be built. Getting closer to lose your short time. Reality is beginning to make itself obvious.

ReplyDeleteYou are right that the wholesale price is just one source of income. Without capacity payments, most power plants would probably go bust. There are also other payments that generators can use to recover their costs such as Make Whole Payments.

DeleteOn your second point, I think regardless of how much wind energy is generated, some form of gas generation will be required to run baseload so under current system the cost of gas will still set the wholesale price.

http://blogs.lse.ac.uk/lsee/2015/03/26/south-east-europe-has-the-ingredients-to-become-the-energy-generation-and-storage-powerhouse-of-europe/

ReplyDelete